📋 Market Research Report | Electronics | SKU: PMR-52246

Global Industrial Sensors Market Size & Forecast to 2032

Industry Analysis, Sensor Types, Key Players, Industry 4.0 Growth Drivers & Demand Forecast to 2032

A comprehensive, data-driven analysis of the global industrial sensors landscape covering temperature, pressure, flow, level, and position sensor technologies alongside IIoT integration, predictive maintenance adoption, and competitive intelligence across North America, Europe, and Asia-Pacific.

Last Updated: May 15, 2026 | Base Year: 2025 | Forecast: 2026–2032 | SKU: PMR-52246

Market Overview & Key Statistics

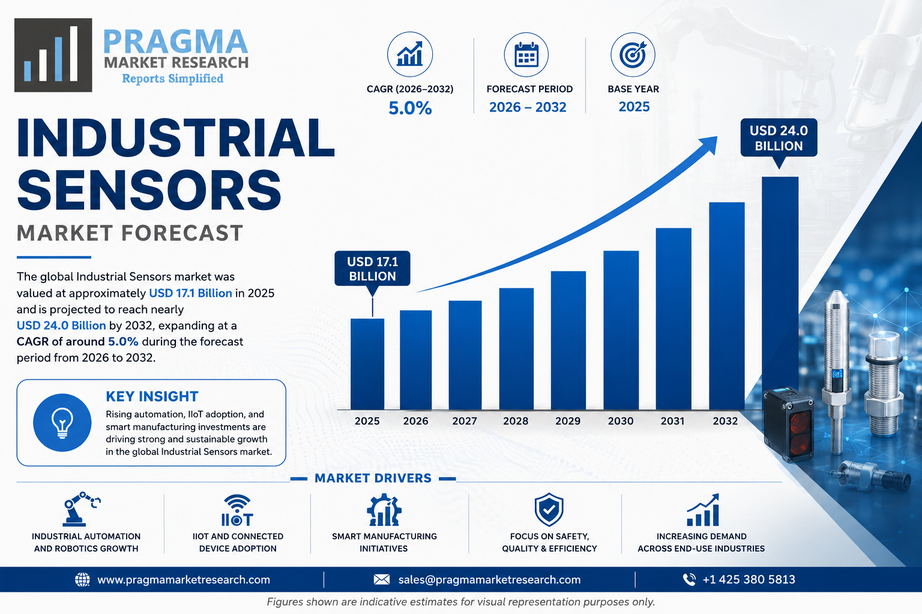

Figure 1: Global Industrial Sensors Market Production Value (USD Million), 2021–2032. Source: Pragma Market Research (PMR-52246)

The Global Industrial Sensors Market was valued at approximately USD 17.1 billion in 2025 and is projected to reach nearly USD 24.0 billion by 2032, expanding at a CAGR of around 5.0% during the forecast period 2026 to 2032. Growth is being driven by the accelerating adoption of industrial automation, widespread deployment of Industry 4.0 architectures, and rising investment in real-time process monitoring and predictive maintenance across manufacturing, oil and gas, energy, and chemical industries globally. The International Energy Agency (IEA) has highlighted industrial digitalization of which sensing and monitoring infrastructure is a foundational layer as one of the most significant near-term levers for industrial energy efficiency improvement.

Key Insight: As factories move from periodic inspection to continuous, sensor-driven operational intelligence, industrial sensors market are shifting from commodity components to strategic infrastructure with purchasing decisions increasingly influenced by connectivity standards, cybersecurity compliance, and software ecosystem compatibility rather than measurement specification alone.

Industrial sensors occupy a foundational position in modern manufacturing and process control infrastructure. Every automated assembly line, every chemical reactor operating under controlled conditions, every wind turbine monitored for performance degradation depends on a network of sensors converting physical phenomena into actionable data. The integration of these devices into Industrial IoT (IIoT) ecosystems has fundamentally changed their value proposition transforming them from local measurement instruments into nodes in a real-time data fabric that feeds SCADA systems, digital twins, and AI-driven analytics platforms.

The U.S. Department of Commerce and the National Institute of Standards and Technology (NIST) have both identified sensor interoperability and data standards as critical enablers of the smart manufacturing transition. Standards bodies including ISA (International Society of Automation) and IEC are actively developing frameworks that govern sensor communication protocols, calibration requirements, and functional safety classifications creating a structured compliance environment that is influencing procurement specifications across global industrial sectors.

What Are Industrial Sensors?

Industrial sensors are electronic measurement devices designed to detect, quantify, and transmit data about physical parameters including temperature, pressure, flow rate, level, position, proximity, vibration, and chemical composition within industrial processes and environments. Unlike consumer-grade sensors, industrial variants are engineered for continuous operation under demanding conditions: extreme temperatures, corrosive atmospheres, high-pressure environments, electromagnetic interference, and physical shock or vibration. They are built to meet stringent accuracy, repeatability, and longevity requirements that consumer electronics cannot satisfy.

Modern industrial sensors are increasingly designed with integrated signal processing, digital communication interfaces (HART, IO-Link, Profibus, EtherNet/IP, OPC UA), and self-diagnostic capabilities. Sensors used in safety-critical applications must comply with functional safety standards such as IEC 61508 (general) and IEC 61511 (process industries), while those deployed in hazardous areas require ATEX (Europe) or NEC Class/Division (North America) certification. The shift toward wireless sensor networks using protocols including WirelessHART, ISA100.11a, and Bluetooth Low Energy is enabling instrumentation of previously inaccessible plant locations, significantly expanding the addressable scope of industrial monitoring programs.

Key Growth Drivers

Industry 4.0 and Industrial Automation Reshaping Sensor Demand

The most powerful structural force behind this market is the global transition toward smart, connected industrial operations. Industry 4.0 as defined by the German federal government's original initiative and now embraced by industrial policy frameworks worldwide places sensor-based real-time monitoring at the core of the intelligent factory concept. Every robotic arm, every automated guided vehicle, every process reactor operating under closed-loop control requires multiple sensor inputs to function as designed. The proliferation of collaborative robots (cobots), flexible manufacturing cells, and automated quality inspection systems is generating proportional growth in sensor procurement volumes that shows no sign of plateauing.

The US Manufacturing USA network, Germany's Industrie 4.0 platform, and China's Made in China 2025 framework have all created structured investment pipelines supporting smart factory development and each of these programs directly stimulates industrial sensor procurement as a foundational technology layer. The industrial automation services market is growing in parallel, with system integrators specifying advanced sensor configurations as standard components of automation upgrade projects.

Predictive Maintenance and Real-Time Monitoring Driving IIoT Adoption

The business case for predictive maintenance avoiding unplanned equipment failures by identifying degradation signatures before failure occurs is well established and widely accepted across heavy industry, energy, and process manufacturing. The sensor infrastructure required to support predictive maintenance programs includes vibration sensors for rotating equipment health monitoring, temperature sensors tracking thermal anomalies in electrical systems and bearings, and pressure/flow sensors identifying process deviations that indicate developing faults. Investment in this sensor layer is a prerequisite for any meaningful predictive maintenance capability, creating a structurally embedded demand channel as industrial operators upgrade from time-based to condition-based maintenance strategies.

Cloud-connected IIoT platforms from Siemens (MindSphere), Honeywell (Forge), ABB (Ability), and Rockwell Automation (FactoryTalk) are accelerating sensor deployment by making it easier to connect, aggregate, and analyze data from distributed sensor networks without custom integration work. These platform ecosystems effectively create a "network effect" for sensor adoption each new sensor connected to the platform increases the analytical value of the overall dataset, incentivizing operators to instrument progressively more asset types and process points.

Expanding Applications in Energy, Oil & Gas, and Chemical Industries

Beyond manufacturing, industrial sensors are seeing robust demand growth across the energy transition and process industries. In oil and gas, upstream production monitoring, pipeline integrity management, and refinery process control all depend on extensive sensor networks. The energy transition is simultaneously creating new demand categories sensors for wind turbine condition monitoring, solar inverter performance tracking, electrolyzer control in green hydrogen production, and grid stability monitoring in battery energy storage systems. These emerging applications require specialized sensor configurations that established manufacturers and innovative new entrants are actively developing.

The chemical industry's increasing focus on process intensification producing more output from smaller, more efficient reactors operating closer to their thermodynamic limits is creating demand for higher-accuracy, faster-response sensors that can manage tighter control tolerances. Regulatory requirements for environmental emissions monitoring under EPA and EU Industrial Emissions Directive frameworks are also mandating sensor deployments for continuous emissions monitoring systems (CEMS) at an expanding range of industrial facilities.

MEMS Technology and Miniaturization Broadening Market Accessibility

Microelectromechanical systems (MEMS) technology has dramatically reduced the cost and size of many sensor types particularly pressure, inertial, and gas sensors enabling deployment in applications where the economics previously didn't justify instrumentation. MEMS-based pressure sensors that cost a fraction of traditional piezoelectric alternatives have opened up mid-market manufacturing and building automation segments to comprehensive sensing strategies. Combined with advances in low-power wireless communication and coin-cell battery longevity, MEMS miniaturization is enabling "sensor everywhere" deployment philosophies that were technically and economically impractical a decade ago.

Market Segmentation

The report analyses the global industrial sensors market across two primary segmentation dimensions sensor type and end-use application providing production volume, production value, and average pricing data for each category from 2021 through 2032.

By Sensor Type

Temperature Sensors

Pressure Sensors

Flow Sensors

Level Sensors

Position Sensors

Others

By Application

Manufacturing

Energy & Power

Oil & Gas

Chemical

Mining

Others

By Connectivity

Wired (4–20mA, HART)

Fieldbus (Profibus, FF)

Industrial Ethernet

Wireless (WirelessHART, ISA100)

By End-User

Process Industries

Discrete Manufacturing

Utilities & Infrastructure

Mining & Metals

Temperature Sensors: The Largest Sensor Type Segment

Temperature sensing is the most ubiquitous measurement requirement across industrial operations from process temperature control in chemical and food manufacturing to motor winding protection in rotating equipment and exhaust gas monitoring in energy systems. Temperature sensors accordingly command the largest share of overall industrial sensor revenue. RTDs (resistance temperature detectors), thermocouples, and infrared non-contact sensors are the dominant technologies, with infrared sensing seeing the fastest growth as remote, non-intrusive measurement becomes increasingly preferred in harsh process environments and safety-critical applications.

Pressure Sensors: Fastest-Growing Sensor Type

Pressure sensors are the fastest-growing segment within industrial sensor types, driven by their dual role in both process measurement and machinery health monitoring. MEMS-based pressure sensor technology has brought manufacturing costs down sharply while improving accuracy and expanding the operating range enabling deployment at points in the process that previously relied on manual gauges or infrequent sampling. The oil and gas, chemical, and water/wastewater treatment sectors are generating particularly strong demand for pressure sensing as continuous monitoring requirements expand under regulatory and operational efficiency mandates.

Manufacturing: Dominant Application Segment

The manufacturing sector accounts for the largest share of industrial sensor consumption, driven by the rapid spread of automation, robotics, and smart factory systems across discrete and process manufacturing alike. Automotive, electronics, food and beverage, pharmaceutical, and general industrial manufacturing are all investing heavily in sensor infrastructure as part of broader digital transformation programs. For investors and industry participants evaluating the broader industrial automation services market, the manufacturing application segment is the primary demand anchor that will sustain above-average sensor market growth through the forecast period.

Access the Complete 242-Page Research Report

Market sizing, competitive profiles with production data, segment forecasts through 2032, and country-level consumption analysis across 20+ markets.

Regional Analysis - North America, Europe & Asia-Pacific

Figure 2: Global Industrial Sensors Market Consumption Share by Region 2025 vs. 2032. Source: Pragma Market Research (PMR-52246)

🇺🇸 United States & North America

North America holds a significant market share, anchored by the United States' advanced manufacturing ecosystem, high automation penetration, and substantial investment in digital transformation across oil and gas, aerospace, food processing, and pharmaceuticals. Government programs including the Manufacturing USA institutes and Department of Energy's Advanced Manufacturing Office actively fund sensor technology development and deployment for energy efficiency and process optimization. Canada contributes meaningful demand from its mining and energy sectors. The US tariff environment on electronic components particularly those sourced from China is creating procurement strategy shifts that are benefiting North American and European sensor manufacturers.

🇪🇺 Europe

Europe maintains a strong position in both sensor production and consumption, supported by its industrial base in Germany (automotive, machinery), France (chemicals, aerospace), Italy (precision manufacturing), and the broader EU manufacturing sector. Germany's Industrie 4.0 initiative continues to drive smart factory sensor investment, while EU environmental regulations including REACH, the Industrial Emissions Directive, and emerging emissions monitoring requirements mandate continuous sensor-based monitoring across a broad range of industrial processes. The UK's post-Brexit regulatory environment is maintaining broadly equivalent standards to EU requirements for industrial instrumentation.

🌏 Asia-Pacific (Fastest-Growing Region)

Asia-Pacific is the fastest-growing region and is expected to account for an increasing share of global consumption through 2032. China is the world's largest manufacturing economy and the single largest national market for industrial sensors, driven by robotics deployment, electronics manufacturing expansion, and government-backed smart factory initiatives. Japan and South Korea are significant producers and consumers particularly in automotive and electronics manufacturing. India's expanding industrial base, supported by the Production Linked Incentive (PLI) scheme, is creating new demand across pharmaceuticals, electronics, and automotive sectors. Southeast Asia's manufacturing development trajectory adds further regional momentum.

🌍 Middle East, Africa & Latin America

The Middle East and GCC countries generate substantial industrial sensor demand from oil and gas upstream operations, petrochemical facilities, and desalination plants all of which require extensive sensor networks for process control and safety compliance. Israel is a notable market for high-technology sensor applications. Brazil and Mexico are the primary Latin American markets, with Brazil's oil and gas sector (led by Petrobras operations) and automotive manufacturing generating consistent sensor procurement activity. Mexico's manufacturing growth particularly in the automotive and electronics sectors near the US border is supporting demand expansion.

Key Companies & Competitive Landscape

Figure 3: Industrial Sensors Market Competitive Landscape & Revenue Share by Manufacturer (2025). Source: Pragma Market Research (PMR-52246)

The competitive landscape spans global diversified automation conglomerates, specialist sensor technology companies, and innovative niche players serving specific measurement domains. Honeywell leverages its broad industrial instrumentation portfolio and deep relationships with process industry operators to maintain leadership across temperature, pressure, and gas sensing categories. Omron and FANUC compete on the strength of their integrated automation ecosystems where sensors are sold as components of broader robotic and automation systems rather than standalone products. Cognex has built a dominant position in machine vision sensing for automated inspection, a fast-growing category within industrial sensing driven by quality control automation in electronics and automotive manufacturing. AMS brings semiconductor-level miniaturization expertise, particularly for MEMS-based sensing applications.

Specialist innovators are carving out defensible positions in emerging sensing categories. Roboception and Hermary Opto Electronics focus on 3D vision and structured light sensing for robotic guidance applications. FUTEK Advanced Sensor Technology serves high-precision force and torque measurement applications in robotics and aerospace. Tekscan has developed thin-film pressure mapping technology that is finding application in manufacturing quality control and medical device testing. The full competitive analysis including production data, revenue figures (2021–2026), and strategic positioning is available in the complete industrial sensors market report check details and purchase directly here.

Technology Trends & Innovation

AI-Enabled Sensing and Edge Analytics

The integration of machine learning algorithms directly into sensor hardware or at the edge gateway level immediately adjacent to sensors is one of the most consequential technology shifts in this market. Traditional sensors transmit raw measurement data to central control systems for processing; AI-enabled variants perform local inference, transmitting only interpreted results or anomaly alerts. This approach reduces network bandwidth requirements, enables faster response times for time-critical safety applications, and allows sensor networks to function with reduced cloud connectivity in remote or latency-sensitive environments.

In practical terms, an AI-enabled vibration sensor on a rotating machine can distinguish between vibration patterns associated with bearing wear, imbalance, misalignment, and resonance providing a specific diagnostic output rather than raw vibration amplitude data. This shift from data transmission to insight transmission represents a fundamental change in sensor value proposition and is supporting premium pricing for intelligent sensor variants. The infrared sensors market is seeing parallel innovation, with AI-enhanced thermal imaging sensors enabling automated defect detection in manufacturing and predictive maintenance in electrical infrastructure.

Wireless Sensor Networks and IIoT Connectivity Standards

Wireless connectivity is transforming the economics of industrial sensor deployment. Cable installation accounts for a substantial portion of the total cost of a sensor instrumentation project in brownfield facilities sometimes exceeding the cost of the sensors themselves. Wireless protocols including WirelessHART (the dominant standard for process industries), ISA100.11a, and increasingly Bluetooth Low Energy (BLE) and 5G private networks are enabling cost-effective instrumentation of locations that were previously uneconomic to wire.

The emergence of IO-Link as a standardized point-to-point digital communication interface for sensors on machine-level automation systems has been particularly significant for discrete manufacturing. IO-Link enables bi-directional communication, remote parameter setting, and automatic device identification capabilities that significantly simplify maintenance, reduce reconfiguration time during product changeovers, and enable sensor-level diagnostic data in IIoT architectures. The shift toward OPC UA as the interoperability standard for industrial data exchange is also encouraging sensor manufacturers to embed OPC UA server functionality directly in sensor hardware.

Multi-Parameter Sensing and Sensor Fusion

Rather than deploying separate sensors for each measurement parameter, advanced industrial monitoring systems are increasingly combining multiple sensing modalities in single devices or tightly integrated sensor clusters. Multi-parameter transmitters that simultaneously measure temperature, pressure, and flow in a process connection or vibration sensors that incorporate temperature sensing for bearing health assessment reduce installation complexity and cost while providing richer, correlated data for analytics platforms. Sensor fusion algorithms that combine inputs from multiple sensor types to derive higher-level inferences about machine or process state are a key area of active development, particularly for predictive maintenance and automated quality inspection applications that benefit from the broader sensor market trend toward integrated measurement architectures.

Opportunities & Market Challenges

Where the Growth Opportunities Are Concentrated

The retrofit market in established industrial facilities represents a significant near-term commercial opportunity. A large proportion of the global installed base of manufacturing and process plants was built before comprehensive digital instrumentation was economically or technically feasible. As these operators modernize to support IIoT analytics, predictive maintenance, and energy efficiency programs, they are installing sensor infrastructure at points that previously had no instrumentation. This retrofit wave is generating sensor procurement volumes that exceed greenfield construction activity in many mature industrial markets.

The energy transition is creating entirely new application categories for industrial sensing. Green hydrogen production requires specialized sensors for electrolyzer monitoring, hydrogen purity measurement, and leak detection a chemistry portfolio that differs meaningfully from conventional industrial gas applications. Battery energy storage systems require temperature, voltage, and gas sensing for safety monitoring. Carbon capture facilities require precise flow and chemical concentration measurement at multiple process points. These emerging applications represent high-value, technically demanding sensor requirements where price sensitivity is lower than in commoditized general industrial segments.

For investors considering the broader electronics and petrochemical sensors market, industrial sensing offers structurally durable demand driven by regulatory compliance requirements, safety mandates, and operational efficiency incentives that persist regardless of broader economic cycle movements.

Key Market Challenges

Cybersecurity has emerged as a significant constraint on the deployment of connected industrial sensor networks. High-profile attacks on industrial control systems including the Colonial Pipeline incident and attacks on water treatment facilities have heightened awareness of the risks associated with networked industrial infrastructure. The IEC 62443 cybersecurity standard for industrial automation and control systems is increasingly specified by asset owners, but compliance adds cost and complexity to sensor procurement and system integration. Supply chain concentration particularly the dependence of sensor semiconductor manufacturing on Asian foundries has created procurement risk that became highly visible during the 2021–2023 semiconductor shortage and remains a strategic concern for industrial buyers.

Research Methodology & Author

Authored & Reviewed By

AD

Akshay Deshmukh

Senior Market Research Analyst Electronics & Industrial Technology, Pragma Market Research

Akshay specializes in electronics, industrial automation, and sensing technology markets across North America, Europe, and Asia-Pacific. His research covers competitive intelligence, technology adoption analysis, regulatory landscape mapping, and demand forecasting for semiconductor and electronic component markets serving process and discrete manufacturing industries.

Primary Research: In-depth interviews with sensor manufacturers, industrial automation integrators, plant engineers, procurement managers, and technology investors across the US, Germany, Japan, China, and India.

Secondary Research: Analysis of company financial filings, trade data, ISA and IEC standards publications, IEA industrial digitalization reports, and manufacturing industry association data.

Market Estimation: Top-down and bottom-up triangulation across production capacity data, component import/export statistics, application-level consumption analysis, and pricing trends by sensor type.

Validation: Preliminary findings reviewed with industrial instrumentation domain experts and cross-referenced against trade association benchmark data and company-reported revenue figures before publication.

What is the current size of the Global Industrial Sensors Market?+

The Global Industrial Sensors Market was valued at approximately USD 17.1 billion in 2025 and is projected to reach nearly USD 24.0 billion by 2032, expanding at a CAGR of around 5.0% during the forecast period 2026–2032. The report uses 2025 as the base year with coverage spanning five major regions and 20+ countries. Growth is driven by industrial automation adoption, Industry 4.0 implementation, and rising demand for IIoT-enabled predictive maintenance solutions.

What are industrial sensors and what role do they play in smart manufacturing?+

Industrial sensors are purpose-built electronic measurement devices that detect physical parameters including temperature, pressure, flow, level, and position and convert them into signals for control systems, SCADA platforms, or IIoT analytics engines. In smart manufacturing, sensors form the data acquisition foundation of the Industry 4.0 stack, enabling real-time process monitoring, automated quality control, predictive maintenance, and digital twin modeling. The accuracy, connectivity, and reliability of sensor infrastructure directly determines the effectiveness of any industrial automation or data analytics initiative.

Which regions have the strongest demand for industrial sensors?+

North America and Europe hold the largest market shares, driven by high industrial automation penetration and significant digital transformation investment in manufacturing and process industries. The US leads North America, while Germany, France, and Italy are the most active European markets. Asia-Pacific is the fastest-growing region, with China, Japan, South Korea, and India all generating strong demand growth. China is the largest single national market by consumption volume. The Middle East and GCC countries are important demand centres for oil and gas and petrochemical sensor applications.

What standards apply to industrial sensors?+

Sensors in hazardous environments require ATEX (EU) or NEC/IECEx certification. IEC 61508 and IEC 61511 govern functional safety for sensors in safety-instrumented systems. ISA standards cover process instrumentation performance and installation. For IIoT-connected sensors, IEC 62443 cybersecurity standards are increasingly specified by industrial buyers. In the US, OSHA PSM regulations under 29 CFR 1910.119 require reliable instrumentation for covered chemical processes. Calibration requirements are governed by ISO/IEC 17025 standards for testing and calibration laboratories.

Who are the leading companies in the industrial sensors market?+

The report profiles Honeywell, FANUC, Cognex, Omron, ATI Industrial Automation, EPSON, AMS, FUTEK Advanced Sensor Technology, OTC Daihen, Roboception, Tekscan, Hermary Opto Electronics, MaxBotix, iniLabs, and Perception Robotics. Each profile includes company details, product portfolio, production and revenue data (2021–2026), pricing analysis, and recent strategic developments including mergers, acquisitions, and technology launches.

How can I access or purchase this report?+

The 242-page report (SKU: PMR-52246) is available at https://www.pragmamarketresearch.com/reports/52246/global-industrial-sensors-market-research-report-2022. You can request a free sample, purchase a single-user license from USD 3,500, or contact the team at sales@pragmamarketresearch.com or +1 425 380 5813 for multi-user or custom research options.

Production & consumption analysis by region and country

20+ country consumption forecasts

15 company profiles with production & revenue data

Market share by manufacturer (Tier 1/2/3 classification)

Market drivers, restraints, challenges, and opportunities

Impact analysis of US tariff policies on the market

Industry value chain & supply chain analysis

149 data tables · 72 market figures

PDF and Excel delivery formats

Post-purchase analyst access

► Benchmark production capacity, revenue share, and pricing data against 15 key competitors in the global industrial sensors space.

► Identify sensor type and application segments offering the strongest near-term growth through 2032.

► Understand regional demand dynamics across North America, Europe, and Asia-Pacific and how tariff and trade policies are reshaping procurement strategies.

► Evaluate technology investment priorities from AI-enabled sensing to wireless IIoT connectivity for R&D and product roadmap decisions.

► Support business development, M&A due diligence, and strategic planning with independent third-party market intelligence.

Client Reviews

4.6

★★★★★

29 verified client ratings | Out of 5

★★★★★

"Excellent depth on temperature and pressure sensor segments. The competitive benchmarking data saved us weeks of primary research and gave us exactly the product positioning context we needed."

Sven L.

·

★★★★☆

"Solid market sizing data and good regional coverage for Asia-Pacific. The application segment breakdown by industry was well-structured and directly useful for our business planning process."

Meera P.

·

★★★★★

"The technology trends section on AI-enabled sensing and wireless IIoT protocols was the most current analysis I've seen on this topic. Well worth the investment for anyone evaluating the sensor market seriously."