📋 Market Research Report | Energy Sector | SKU: PMR-121677

Global Battery Energy Storage System Fire Protection Market Size & Forecast 2032

Industry Analysis, Market Share, Key Players, Growth Drivers & Forecast to 2032

A comprehensive, data-driven analysis of the BESS fire protection landscape covering fire suppression systems, detection technologies, regulatory dynamics, regional demand patterns, and competitive intelligence across the United States, Europe, and the Middle East.

Last Updated: April 20, 2026 | Base Year: 2025 | Forecast: 2026–2031 | SKU: PMR-121677

Market Overview & Key Statistics

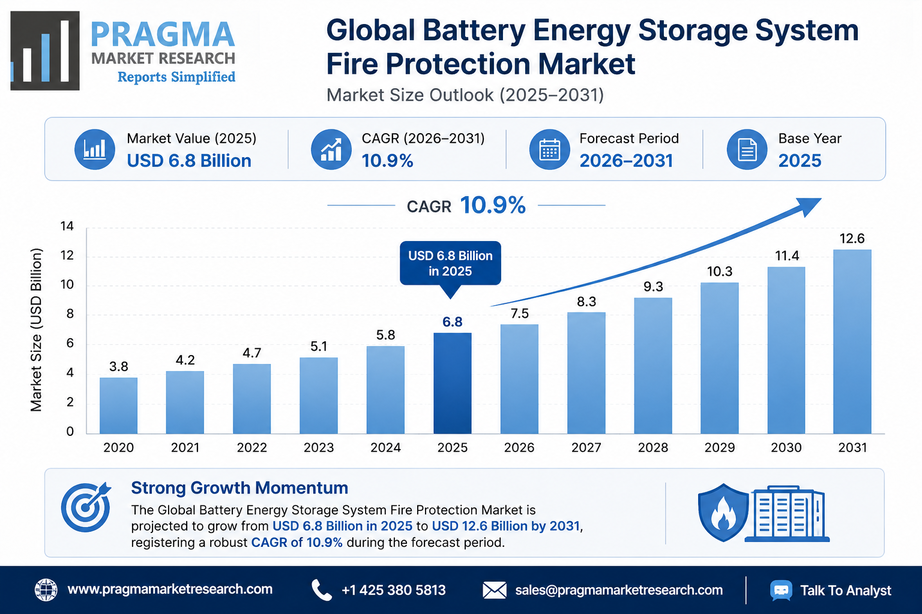

Figure 1: Global Battery Energy Storage System Fire Protection Market Revenue (USD Million), 2020–2031. Source: Pragma Market Research (PMR-121677)

The Global Battery Energy Storage System (BESS) Fire Protection Market was valued at USD 6.8 billion in 2025 and is on track to expand at a compound annual growth rate of 10.9% from 2026 to 2031. Demand is being shaped by the accelerating global buildout of grid-connected battery storage, increasingly stringent fire safety standards including NFPA 855 in the United States and meaningful advances in early-detection technology that are changing how operators think about battery fire risk.

Key Insight: As the global energy storage market scales toward terawatt-hour deployments, fire safety has shifted from a compliance checkbox to a core investment consideration influencing project financing, insurance structures, and long-term asset valuations across the US, Europe, and the Middle East.

Battery energy storage is now critical infrastructure integral to renewable energy integration, frequency regulation, and grid resilience programs across every major electricity market. But the lithium-ion chemistry powering most modern BESS installations introduces a specific hazard: thermal runaway. When a cell overheats due to internal short circuits, mechanical damage, or overcharging, the resulting self-sustaining reaction can propagate across adjacent modules with remarkable speed. The gases released are toxic, flammable, and partially self-oxidizing which is why traditional water-based suppression systems offer limited protection. This has generated a specialized and rapidly growing segment of safety solutions built specifically for battery environments.

Data from the U.S. Department of Energy and the International Energy Agency (IEA) indicates global grid-scale battery capacity is set to multiply significantly by the end of this decade. Each new gigawatt-hour of storage capacity brings a corresponding requirement for certified fire protection creating durable, embedded demand that this report quantifies across geographies, product segments, and competitive positions.

What Is Battery Energy Storage System Fire Protection?

BESS fire protection encompasses the integrated set of systems and protocols designed to detect, prevent, and suppress fire events within battery energy storage installations. Unlike standard industrial fire safety, these solutions must address the unique behavior of lithium-ion and related battery chemistries particularly the risk of thermal runaway propagation, the release of toxic off-gases well before any visible flame, and the re-ignition tendency that limits conventional suppression agent effectiveness.

A complete safety architecture for a modern BESS facility typically includes multi-gas early-detection sensors, thermal imaging or heat-flux monitoring, dedicated suppression agents (clean agents, high-pressure water mist, inert gas systems), fire-rated enclosure materials, and automated response platforms integrated with the Battery Management System and SCADA infrastructure. UL 9540 certification has become a de facto requirement in the US and is increasingly expected in European markets particularly for projects seeking commercial financing or grid connection approval.

Key Growth Drivers

Battery Storage Deployments Are Scaling Fast

Solar and wind generation are intermittent by nature and paired battery storage has become the preferred solution for managing that variability at grid scale. The US Inflation Reduction Act has unlocked substantial new storage project pipelines across multiple states. Europe's energy security drive following recent geopolitical disruptions has created similar procurement momentum continent-wide. Gulf Cooperation Council nations are committing to large-scale solar-plus-storage projects as part of broader economic diversification programs. Each installation requires certified fire protection, creating what amounts to a structurally captive demand channel tied directly to the broader renewable energy market.

Regulatory Frameworks Are Solidifying

The compliance environment for BESS fire safety is maturing across all major markets. In the US, NFPA 855 has established minimum requirements for detection, suppression, separation distances, and operational safety management conditions that local authorities are increasingly enforcing as prerequisites for permit approval. Insurance underwriters, particularly those active in the Lloyd's of London market, are layering additional requirements on top of the regulatory baseline, effectively raising the bar on what constitutes acceptable protection for any bankable storage project.

Detection Technology Has Made a Meaningful Leap

Early-warning detection is advancing quickly. Traditional smoke detectors trigger only after ignition at which point suppression options are constrained and asset damage may already be severe. Multi-gas electrochemical sensors now detect hydrogen, carbon monoxide, and volatile organic compounds that a battery cell releases during the early stages of thermal stress sometimes hours before any visible combustion. Some platforms integrate these sensors with AI-driven anomaly detection running against live BMS data streams, enabling operators to isolate affected modules before the situation escalates. This pre-fire philosophy is reshaping procurement criteria across North America and Europe.

Asset Owners Are Treating Fire Safety as a Financial Priority

A utility-scale battery storage facility typically represents an investment running into tens or hundreds of millions of dollars. A major fire event can result in total asset loss, extended downtime, regulatory penalties, and years of litigation none of which project finance lenders or equity sponsors are prepared to accept without adequate mitigation. Robust, independently certified fire protection has become a bankability factor, linking procurement spend on safety systems directly to the broader investment cycle in energy infrastructure.

Market Segmentation

The report provides granular revenue analysis across four primary dimensions, giving stakeholders a clear view of where demand is concentrating and where the strongest growth pockets lie through 2031.

By Product Type

Fire Suppression Systems

Fire Detection Systems

Fire Extinguishers

Others (Passive, Monitoring)

By Application

Utility-Scale

Commercial

Industrial

Residential

By Battery Chemistry

Lithium-Ion

Lead-Acid

Flow Batteries

Others

By End-User

Energy Sector

Automotive

Manufacturing

Others

Suppression Systems: The Largest Product Segment

Fire suppression accounts for the largest share of overall market revenue encompassing gaseous clean agents, high-pressure water mist systems calibrated to cool battery cells without triggering conductive short circuits, and aerosol-based solutions suited to containerized enclosures. The segment draws from both new-installation demand and a growing retrofit pipeline as operators of older BESS facilities upgrade to current safety standards.

Detection Systems: Fastest-Growing Segment

Fire detection and early-warning platforms are expanding faster than any other category. The industry-wide shift toward pre-fire intervention detecting thermal stress before ignition rather than reacting after the fact commands significantly higher average selling prices and generates recurring revenue through maintenance and software licensing. This segment is attracting disproportionate R&D investment from most major players in the space.

Utility-Scale: Dominant by Application

Containerized BESS units require dedicated protection for each individual container as well as facility-level systems, creating a multiplication effect on per-project fire safety spend. The utility-scale energy storage market therefore drives a disproportionately large share of total demand, even if residential adoption is growing faster in percentage terms.

Access the Complete 210-Page Research Report

Market sizing, company profiles, segment forecasts through 2031, and country-level data across 20+ markets available immediately.

Figure 2: BESS Fire Protection Market Share by Region 2025 vs. 2031 Comparison. Source: Pragma Market Research (PMR-121677)

United States & North America

North America holds the largest regional share, with the US as the primary demand centre. Federal clean energy legislation has unlocked major new storage pipelines across California, Texas, Florida, and the mid-Atlantic corridor. NFPA 855 compliance creates a well-defined regulatory floor, while state-level storage mandates add further project velocity. The commercial and industrial segments are also gaining traction as corporations pursue energy resilience and behind-the-meter storage strategies.

Europe

The second-largest and most complex region from a regulatory standpoint. The UK has built one of the world's most advanced grid-scale battery portfolios, with dedicated BESS fire guidance from the National Fire Chiefs Council. Germany, France, and Spain are active under their respective energy transition programs. Europe's energy security priorities are structurally elevating demand for domestic storage capacity and the safety infrastructure that protects it.

Middle East & Africa

The fastest-growing region and arguably the most demanding operating environment. Saudi Arabia's Vision 2030 and Abu Dhabi's clean energy programs are generating significant utility-scale BESS procurement. High ambient temperatures in Gulf climates accelerate battery degradation and elevate thermal runaway risk making fire protection systems not just a regulatory requirement but an operational imperative. South Africa's grid challenges are also driving rapid BESS adoption.

Asia-Pacific

China, Australia, India, Japan, and South Korea collectively represent a large and growing share of global storage deployment. China's role as both the world's largest BESS market and a dominant manufacturer creates a complex dynamic for international fire safety suppliers. Australia's extraordinary storage growth has made it a key demand centre for both residential and utility-scale fire protection solutions.

Key Companies & Competitive Landscape

Figure 3: BESS Fire Protection Market Competitive Landscape & Revenue Share Rankings (2025). Source: Pragma Market Research (PMR-121677)

Johnson ControlsSiemens AGHoneywell InternationalABB Ltd.Schneider Electric SEEaton CorporationTyco InternationalKidde Fire SystemsMinimax Viking GmbHHalma plc

The competitive field includes diversified global conglomerates and focused fire protection specialists. Johnson Controls and Siemens AG leverage their integrated building automation and energy management ecosystems to position fire safety as part of a broader operational platform. Honeywell International has invested in AI-assisted detection tools calibrated specifically to battery environments. Schneider Electric and ABB integrate fire safety within their end-to-end power conversion and energy management solutions for large-scale BESS projects.

Specialists like Minimax Viking GmbH and Kidde Fire Systems compete on suppression chemistry innovation, pre-engineered containerized protection packages, and certification programs aligned with evolving NFPA and EN standards. The full competitive analysis company financials, product portfolios, recent M&A, and strategic positioning is covered in the complete market research report check the details and purchase directly here.

Technology Trends & Innovation

Moving Detection Upstream of Ignition

The most consequential shift in this space is the migration from post-ignition detection to pre-fire gas sensing. Multi-gas electrochemical sensors now detect hydrogen, CO, and volatile organic compounds released during the early thermal stress phase of a lithium-ion cell sometimes hours before any visible combustion. When paired with real-time BMS data, these platforms can isolate the affected module and initiate controlled discharge before the event escalates. This pre-fire approach has fundamentally changed how sophisticated asset owners think about battery fire risk.

Suppression Chemistry Designed for Battery Environments

Standard suppression methods are poorly matched to lithium-ion fires. Water exacerbates electrolyte reaction risks, CO₂ offers limited effectiveness against deep-seated cell fires, and halon alternatives face regulatory restrictions in many jurisdictions. The industry is converging on high-pressure water mist for external cooling, fluorinated ketone clean agents for enclosed enclosure protection, and passive fire-resistant barrier materials that limit inter-module propagation. Some advanced suppliers in the fire suppression systems market are also exploring direct cell-level liquid cooling to address thermal events at the source.

Connected Monitoring and Remote Response

Many BESS facilities are located in remote or unmanned sites grid connection points, solar farms, offshore substations. IoT-connected sensor networks, cloud-linked SCADA integration, and automated emergency response protocols that can alert fire services and initiate suppression without human intervention are now standard specifications for large-scale projects across North America and Europe.

Opportunities & Market Challenges

Where Suppliers and Investors Should Be Looking

For suppliers with the right certifications and integration capabilities, this market offers revenue visibility tied directly to one of the decade's most durable infrastructure investment themes. The utility-scale segment in the US and UK provides near-term, high-value project revenue for established players. The Middle East represents a series of large single-project opportunities for companies able to engineer solutions around extreme climate conditions.

There is also an underappreciated retrofit opportunity. Many early-generation BESS installations commissioned before current fire safety standards were fully codified lack adequate protection and face mounting pressure from insurers and regulators to upgrade. This segment is addressable with standardized, cost-optimized packages and represents meaningful incremental revenue that doesn't require winning greenfield mandates.

For investors evaluating the smart grid infrastructure market, fire protection for BESS is an attractive niche: structurally essential, regulatory-driven, relatively insensitive to commodity price cycles, and defensible for companies with battery-specific technology moats.

Challenges Worth Noting

Cost remains the primary friction point. Comprehensive protection adds meaningfully to project capital costs, and developers optimizing for levelized cost of storage face real budget pressure. Suppliers must make a compelling total cost of ownership argument including insurance premium reduction data to overcome resistance. Regulatory fragmentation across national markets also creates certification burdens for companies seeking to operate globally.

Research Methodology & Author

Authored & Reviewed By

AD

Akshay Deshmukh

Senior Market Research Analyst Energy & Power Sector, Pragma Market Research

Akshay specializes in energy storage, fire safety infrastructure, and power sector technology markets across North America, Europe, and the Middle East. His research covers regulatory landscape analysis, competitive intelligence, and demand forecasting for grid-scale and distributed energy systems.

Primary Research: In-depth interviews with BESS project developers, fire protection integrators, safety engineers, regulatory officials, and institutional investors across the US, Europe, and Middle East.

Secondary Research: Analysis of regulatory filings, project disclosures, industry association data, IEA storage tracking, DOE publications, and company financial statements.

Market Estimation: Combined top-down and bottom-up methodology, triangulated across supply-side revenue data, project pipeline analysis, and demand-side procurement intelligence.

Validation: Preliminary findings reviewed by domain experts and cross-referenced against publicly available benchmark data before publication.

Reference Sources & Standards

NFPA 855 Standard for the Installation of Stationary Energy Storage Systems

UL 9540 Standard for Energy Storage Systems and Equipment

Frequently Asked Questions

What is the current size of the BESS fire protection market?+

The global market was valued at approximately USD 6.8 billion in 2025 and is projected to grow at a CAGR of 10.9% from 2026 to 2031. The report uses 2025 as the base year with forecasts running through 2031, covering five major regions and 20+ countries.

What is thermal runaway and why does it matter for battery storage?+

Thermal runaway is a self-sustaining exothermic reaction that occurs when a lithium-ion cell overheats beyond a critical threshold. It generates extreme temperatures, releases toxic and flammable gases, and can spread across adjacent modules. Because the process is partially oxygen-independent, conventional suppression agents are often insufficient making specialized pre-fire detection and battery-specific suppression essential for BESS installations.

Which regions drive the most demand for BESS fire safety systems?+

North America primarily the United States holds the largest market share, driven by NFPA 855 compliance requirements and significant utility-scale storage buildout. Europe follows, with the UK, Germany, and France as the most active markets. The Middle East (Saudi Arabia, UAE) is growing fastest, powered by large clean energy programs where extreme ambient temperatures add additional battery fire risk.

What regulations govern BESS fire protection in the US and Europe?+

In the United States, NFPA 855 and UL 9540 are the primary reference standards, with local AHJ requirements varying by jurisdiction. European projects navigate a combination of IEC 62933, EN fire safety standards, and national building codes. The UK's National Fire Chiefs Council has published specific BESS guidance. Insurance underwriters in both markets are also setting de facto requirements above the regulatory floor.

Who are the leading companies in this space?+

The report profiles Johnson Controls, Siemens AG, Honeywell International Inc., ABB Ltd., Schneider Electric SE, Eaton Corporation, Tyco International, Kidde Fire Systems, Minimax Viking GmbH, and Halma plc. Each profile covers financial data, product portfolios, recent strategic developments, and competitive positioning.

How do I access or purchase this report?+

The 210-page report (SKU: PMR-121677) is available at https://www.pragmamarketresearch.com/reports/121677/global-battery-energy-storage-system-fire-protection-market. Request a free sample, purchase directly, or contact the team at sales@pragmamarketresearch.com or +1 425 380 5813 for custom research options.

► Make strategic decisions backed by quantitative market data and forward-looking revenue analysis.

► Understand regulatory dynamics across the US, Europe, and Middle East and their procurement implications.

► Identify which product segments and geographies offer the strongest near-term growth potential.

► Assess competitive positioning against the ten most active players in the global fire protection landscape.

► Support capital allocation decisions with independent third-party market intelligence.

Client Reviews

4.7

★★★★★

38 verified client ratings | Out of 5

★★★★★

"Very thorough coverage of the US and European markets. The segment-level data and company profiles gave our team exactly what we needed for strategic planning."

James R. ·

★★★★☆

"Good depth on the Middle East market, which was difficult to find elsewhere. The thermal runaway section was particularly well-researched and practical."

Aisha M. ·

★★★★★

"The competitive landscape analysis was more detailed than anything we'd seen from other research firms. Worth the investment for anyone evaluating this market seriously."